If you recently opened a home insurance renewal notice and noticed your deductible had changed — or if your agent mentioned something about a new “1% wind and hail deductible” — you probably had a lot of questions and not many answers. Maybe you felt blindsided. Maybe a little frustrated. That reaction is completely understandable, and you are far from the only homeowner in Illinois or Missouri going through this right now.

This is one of the most significant shifts in the home insurance industry in decades, and most homeowners are finding out about it at exactly the wrong time: when they’re holding a renewal letter and trying to figure out what it means for their family’s finances.

This guide is here to change that. By the time you finish reading, you’ll know exactly what’s happening, why it’s happening, what it means in real dollars for your specific situation, and — most importantly — what you can actually do about it.

You’re Not Alone — And You’re Right to Be Concerned

Let’s start here, because this matters: if your home insurance deductible recently changed or is about to change, it is not a mistake, it is not a glitch, and your insurance company did not single you out. This is an industry-wide shift that is affecting homeowners across the Midwest — and it is hitting Illinois and Missouri particularly hard.

Across the region, insurers are moving away from traditional “fixed dollar” deductibles — the kind where you know exactly what you’ll pay ($1,000 or $2,500, for example) — and replacing them with percentage-based wind and hail deductibles. That percentage is typically 1% or 2% of your home’s insured value.

The concern is valid because, as you’ll see in a moment, those percentages translate into real money — often far more than homeowners expect.

What Exactly Is a Wind and Hail Deductible on Home Insurance?

A wind and hail deductible is a specific deductible that applies only when your home suffers damage caused by wind or hail. It is separate from your standard deductible, which applies to other types of claims like fire, water damage, or theft.

Think of it as a second deductible that kicks in specifically for storm-related damage. Your standard deductible might still be $1,000 or $2,500 for most claims, but when a hailstorm damages your roof or high winds tear off siding, your wind and hail deductible is the one that applies — and it is typically much higher.

How Is This Different from the Deductible You’ve Always Had?

The traditional approach was straightforward: you had one deductible for everything. You knew the number, you understood it, and you could plan around it.

The new approach separates wind and hail into its own category with its own, percentage-based deductible. Instead of knowing you’ll pay $2,000 out of pocket if something goes wrong, you now have to calculate what 1% (or 2%) of your home’s insured value amounts to — and for most homeowners in the Metro East area, that number is significantly higher than what they were paying before.

Why Home Insurance Companies Are Making This Change Right Now

This didn’t happen overnight. It’s the result of several years of financial pressure building up in the insurance industry — and the Midwest is squarely at the center of it.

The Real Reason Insurers Are Shifting the Cost to You

Insurance is, at its core, a risk-sharing system. You pay a premium, and your insurer agrees to cover large, unexpected losses. That system works when claims are relatively predictable. When claims become frequent, severe, and expensive — it stops working, at least under the old pricing model.

Between 2022 and 2024, insurance carriers across the country faced an unprecedented wave of weather-related losses. Severe storms, large hail events, and high winds produced billions of dollars in claims — far exceeding what insurers had priced in. For every dollar collected in premiums in some markets, carriers were paying out significantly more in claims. That math is not sustainable for any business.

Rather than simply raising your premium dramatically — or exiting the market entirely, which some carriers have done in other states — many insurers chose a middle path: keeping premiums relatively stable but requiring policyholders to share more of the loss when a wind or hail event occurs. That is the percentage deductible model. It is essentially the insurer saying, “We’ll still be here for the big losses, but you’ll need to cover more of the smaller and mid-size ones.”

Why the Midwest Is Being Hit Harder Than the Rest of the Country

While this trend is national, Illinois and Missouri homeowners are feeling it more acutely than most. The reason is geography. The Midwest sits in the heart of the country’s most severe storm corridor. Hailstorms, tornadoes, and strong convective wind events are not rare occurrences here — they are a regular part of life from spring through fall.

Insurers track every dollar paid in claims by zip code and region. When the data shows that a particular area consistently generates high wind and hail losses, that area gets repriced. The Metro East — including communities like Edwardsville, Glen Carbon, Troy, and Maryville — falls squarely in that category.

That’s not a knock on where you live. It’s simply the reality of why these changes are landing harder here than in, say, the Pacific Northwest.

What a 1% Wind and Hail Deductible Actually Means for Your Wallet

This is where a lot of blogs fall short. They explain the concept but leave you without the actual numbers. Let’s fix that.

Let’s Do the Math: Real Numbers for Illinois and Missouri Homeowners

A percentage deductible sounds abstract until you attach it to a real home value. Here’s what that looks like for homeowners in our area:

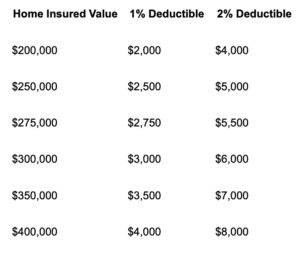

If your home is insured for $275,000 — close to the median insured value in communities like Edwardsville — a 1% wind and hail deductible means you are responsible for the first $2,750 out of pocket before your insurance pays a single dollar on a wind or hail claim. If your insurer has moved to 2%, that number doubles to $5,500.

Now compare that to a traditional fixed-dollar deductible of $1,000 or $2,500. The difference can be significant, especially for a hail event that causes $4,000–$8,000 in roof damage — a very common claim type in this region.

What If Your Insurer Moves to a 2%? Here’s How Much More You’d Owe

Some insurers have gone further than 1%. A handful of carriers are now requiring a 2% wind and hail deductible on new and renewing policies. If your home is insured for $300,000 and your insurer implements a 2% deductible, you are now on the hook for $6,000 before coverage begins.

For a family that planned around a $1,000 or $2,000 deductible, this is a meaningful financial shift — one that needs to be factored into your emergency savings and your overall financial planning.

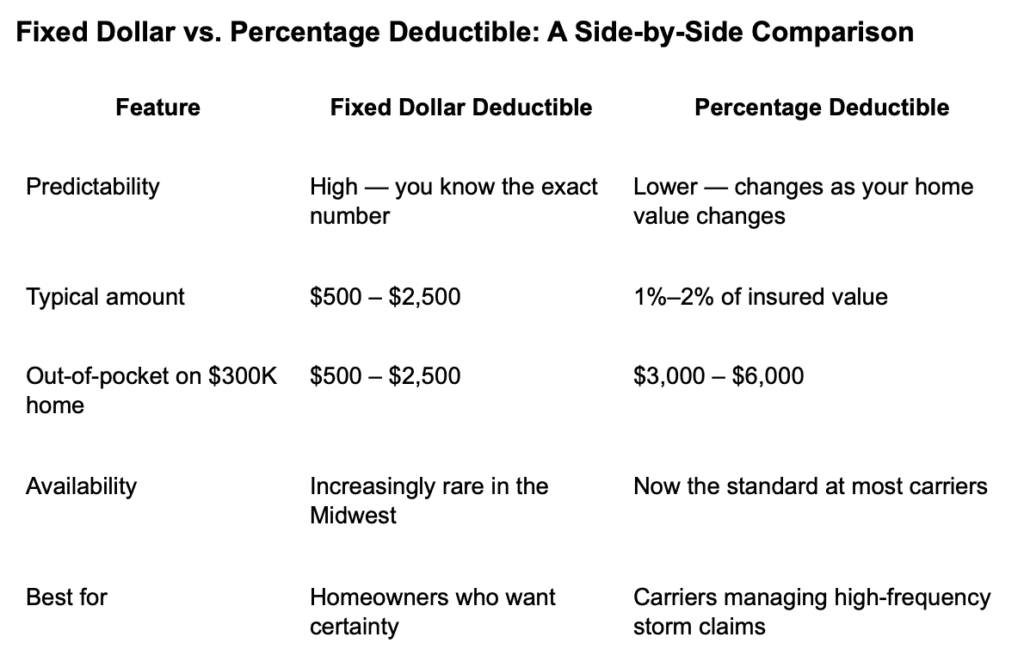

Fixed Dollar vs. Percentage Deductible: A Side-by-Side Comparison

The clear takeaway: fixed-dollar deductibles are friendlier to homeowners in most storm scenarios. Percentage deductibles shift more of the financial risk onto you. Knowing which one your policy currently uses — and what your alternatives are — is essential.

How Your Home Insurance Deductible Can Change — Without You Even Noticing

One of the most frustrating aspects of this shift is how quietly it can happen. Many homeowners in Illinois and Missouri have experienced this change without fully realizing it until after a claim.

New Customers vs. Existing Policyholders: Who Gets Hit First?

Insurers typically roll out these changes in two phases. First, all new customers coming through the door are automatically placed on the new percentage-based deductible. Then, as existing customers come up for renewal, their policies are converted as well.

This means if you’ve been a loyal customer for years, you may not have encountered this yet — but your renewal date could be the moment it arrives. The transition is not optional. If your insurer has made this policy-wide, your renewal will reflect the change whether you asked for it or not.

What Your Renewal Notice Is Actually Telling You (And What It’s Not)

Most renewal notices are dense, technical documents. The change to your wind and hail deductible is often buried in a section called the declarations page or coverage summary — sometimes listed simply as “Wind/Hail Ded: 1%” without further explanation.

What the notice is telling you: your deductible for wind and hail claims is now calculated as a percentage of your dwelling coverage (Coverage A).

What it is not telling you: what that number is in actual dollars, how it compares to what you had before, whether other carriers offer better terms, or what you can do about it.

That gap in communication is exactly why so many homeowners feel blindsided.

Not Every Insurer Is Doing This — And That Changes Everything

Here’s the piece of the story that most people never hear: not every insurance company has moved to a percentage-based wind and hail deductible. And even among those that have, the specific terms — 1% vs. 2%, which perils are included, whether roof age affects the deductible — vary significantly from carrier to carrier.

Some Companies Still Offer Lower or Fixed-Dollar Options

While the industry trend is clearly moving toward percentage deductibles, the market has not fully shifted. Some carriers still offer competitive fixed-dollar deductibles, particularly for well-maintained homes with newer roofs. Others offer 1% as their floor with no movement to 2%. The range of options is wider than your current insurer may lead you to believe.

The challenge is that if you’re working with a single-carrier (captive) agent, they can only offer you what that one company has. If that company has gone to 2%, that’s your only option with them.

This Is Exactly Where an Independent Agent Makes All the Difference

An independent insurance agency — one that represents multiple carriers — can shop the market on your behalf and compare deductible structures, premiums, and coverage terms across many companies simultaneously.

This is a fundamental advantage that often goes unrecognized. Rather than being stuck with whatever one insurer decides, an independent agent can find carriers that still offer more favorable deductible terms for your specific home, location, and coverage needs. Working with an independent insurance agent in Edwardsville means having someone in your corner who is working for you — not for the insurance company.

Don’t Wait for Your Renewal Letter — Take These Steps Now

The single biggest mistake homeowners make is waiting until the renewal lands in the mailbox. At that point, your options are more limited and your timeline is shorter. The homeowners who come out of this shift in the best position are the ones who get proactive 60 to 90 days before their renewal date.

60–90 Days Before Your Renewal: Your Action Checklist

Use this checklist as your guide:

-

Find your current policy’s declarations page. Look specifically for your wind and hail deductible. Is it a fixed dollar amount or a percentage? If it’s a percentage, calculate what it means in actual dollars based on your Coverage A (dwelling) amount.

-

Note your renewal date. Mark it on your calendar and set a reminder for 60–90 days prior.

-

Review your roof’s age and condition. Insurers are increasingly factoring roof age into how they apply deductibles and whether they’ll cover replacement cost vs. actual cash value. A roof over 10–15 years old can significantly affect your options.

-

Check your home’s current insured value. As home values and construction costs have risen, your Coverage A may have been adjusted upward — which means your percentage deductible has grown too, even if the percentage itself hasn’t changed.

-

Contact your insurance agent before renewal, not after. This is the most important step of all.

The Questions You Should Be Asking Your Insurance Agent Right Now

Don’t wait for your agent to bring this up. Come to the conversation prepared with these specific questions:

-

“What is my current wind and hail deductible, and is it a fixed dollar amount or a percentage?”

-

“If it’s a percentage, what does that translate to in actual dollars based on my current Coverage A?”

-

“Is this deductible changing at my next renewal? If so, what will the new amount be?”

-

“Can you show me alternatives — other carriers that may offer a lower or fixed deductible for a similar or better premium?”

-

“Does my current policy cover roof replacement at replacement cost or actual cash value — and is that changing too?”

These questions put you in control of the conversation and ensure you’re making an informed decision rather than simply accepting whatever lands in your mailbox.

How Bundling Your Home and Auto Insurance Could Help Offset the Cost

While bundling won’t change your wind and hail deductible structure itself, it can meaningfully reduce your overall insurance spend — which matters when deductibles are rising. Many carriers offer discounts of 10% to 25% when you combine your home and auto policies with the same company.

If you’re shopping for better wind and hail deductible terms anyway, it’s the perfect time to evaluate bundling your home and auto insurance as part of the same conversation. You may find a carrier that offers both more favorable deductible terms and a meaningful multi-policy discount — a genuine win on both fronts.

Your Questions Answered: Everything Illinois and Missouri Homeowners Are Asking About Wind and Hail Deductibles

What is a 1% wind and hail deductible and how is it calculated?

A 1% wind and hail deductible means that when your home suffers damage specifically caused by wind or hail, you are responsible for paying 1% of your home’s insured dwelling value (Coverage A) before your insurance company pays anything on that claim. It is calculated by taking your Coverage A amount and multiplying it by 0.01. For example, if your home is insured for $300,000, your 1% wind and hail deductible is $3,000. This applies specifically to wind and hail claims — your standard deductible still applies to all other claim types.

Why did my home insurance deductible change at renewal?

Your deductible changed at renewal because your insurance carrier made a policy-wide decision to move from fixed-dollar deductibles to percentage-based wind and hail deductibles. This is being driven by significant financial losses insurers have absorbed from storm-related claims in the Midwest over recent years. Insurers are required to apply these changes at renewal — they cannot change your deductible mid-policy without your agreement — which is why the renewal date is when most homeowners first notice it.

Can my insurance company raise my deductible without my permission?

In practical terms, yes — at renewal. Your insurance policy is a contract that renews on a set date, and at each renewal, your insurer has the right to change the terms, including your deductible. They are required to notify you of material changes before renewal, typically 30–60 days in advance, which is why that renewal notice is so important to read carefully. However, you are not obligated to renew with that insurer. You have the right to shop for a different policy before your renewal date, which is exactly why reviewing your options 60–90 days in advance is so valuable.

What is the difference between a fixed-dollar deductible and a percentage deductible?

A fixed-dollar deductible is a set, predetermined amount — for example, $1,000 or $2,500 — that you pay out of pocket before insurance covers a claim, regardless of your home’s value. A percentage deductible is calculated as a percentage of your home’s insured value and fluctuates as that value changes. A percentage deductible is almost always higher than a traditional fixed-dollar deductible for most homeowners, and it can grow over time as your home’s insured value is adjusted upward at renewal.

How much will I pay out of pocket with a 1% wind and hail deductible?

Your out-of-pocket cost is 1% of your home’s Coverage A (dwelling) amount. Here are some quick reference figures for common home values in our area: $200,000 home = $2,000 out of pocket; $275,000 home = $2,750; $300,000 home = $3,000; $350,000 home = $3,500; $400,000 home = $4,000. If a storm causes $5,000 in damage to your $300,000 home, you would pay $3,000 and your insurer would cover the remaining $2,000. If the damage is $3,000 or less, you would pay the entire bill yourself since it falls under your deductible.

You Have More Options Than Your Insurance Company Wants You to Think

Here is the most important thing to take away from everything you’ve just read: you are not stuck.

Yes, the industry is changing. Yes, the Midwest is bearing the brunt of it. Yes, percentage-based wind and hail deductibles are becoming the new normal at many carriers. But “many carriers” is not “all carriers” — and even among those that have shifted, there is meaningful variation in how they structure their deductibles, their premiums, and their overall coverage terms.

The homeowners who fare best through this shift are the ones who don’t simply accept the renewal notice as their only option. They are the ones who ask questions, review their coverage proactively, and work with someone who can compare the full market on their behalf.

That is exactly what an independent agency is built to do. Whether you want to understand your homeowners insurance coverage options in full, explore whether a different carrier could offer better deductible terms, or simply get a clear, honest explanation of what your current policy actually says — the team at Hosto Financial is here to help.

We’ve spent over three decades serving homeowners in Edwardsville, Glen Carbon, Troy, Maryville, and the surrounding communities. We don’t work for one insurance company. We work for you.

If your renewal is coming up — or even if it’s months away — now is the right time to have the conversation. Reach out to us today and let’s look at where you stand and what your options really are.